Last week, New Jersey Senators Robert Smith (D) and Christopher Bateman (R) introduced a bipartisan energy bill in the Senate, with a broad coalition of support from solar energy owners, installation and development stakeholders, renewable energy advocates, and other environmental groups. S2276, which was referred to the Senate Environment and Energy Committee upon its introduction on May 23, will adjust New Jersey’s renewable portfolio standard (RPS) to address the impending “solar cliff” of oversupply. In addition, the bill establishes a Solar Energy Study Commission to enable the Garden State to evaluate potential paths and long term solutions for the future of solar policy in the New Jersey.

Under the Solar Act of 2012, New Jersey utilized a “pull forward” mechanism to adjust the RPS so that the increased demand could absorb an excess of SRECs in the market; unfortunately, the mechanism created a “valley of death” starting in Energy Year 2019 (June 2018), with initial impact hitting in EY2017 and EY2018. Based on current build rates, the market may build between 80 MW and 231 MW more than the RPS will require in those years. In the EY2019 to EY2025 years, the market may build between 183 MW and 335 MW in excess of the RPS demand. Under current conditions, it is not until EY2026 that retirement impacts will provide relief to the oversupply.

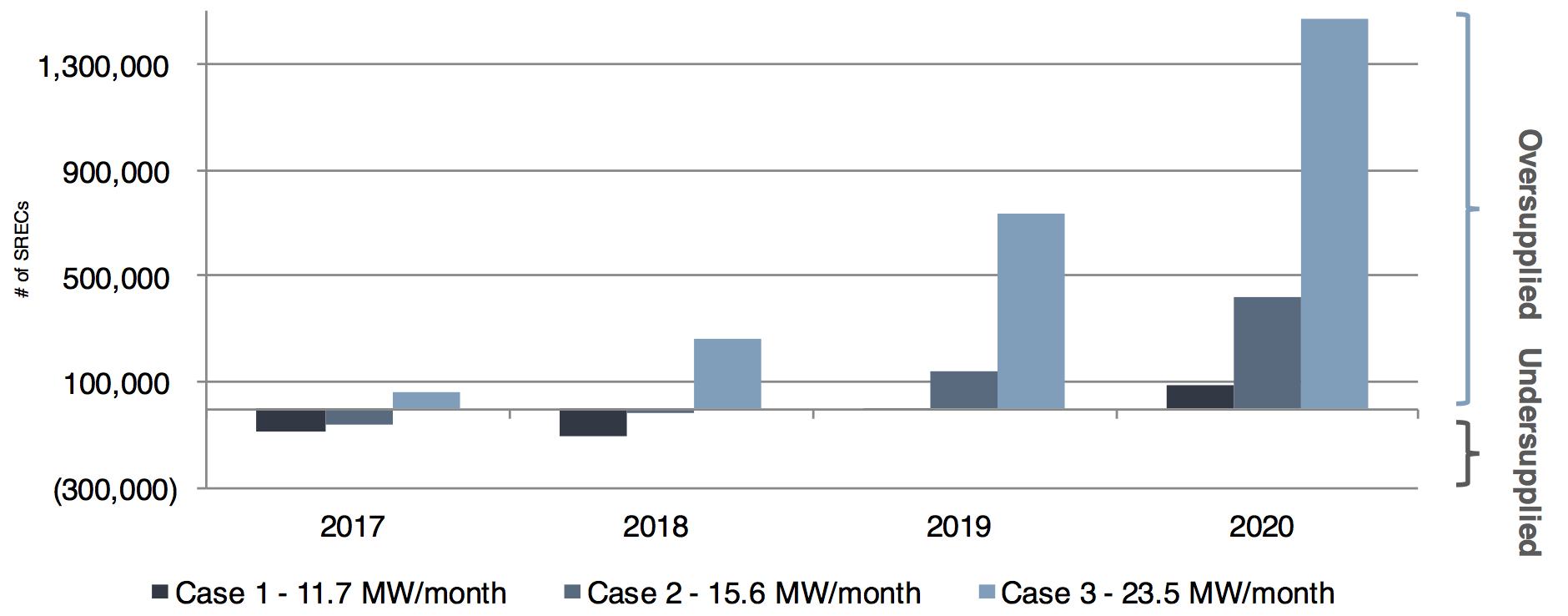

Figure 1 below shows SRECTrade’s projections for three potential capacity growth scenarios, and the resulting oversupply/undersupply, based on the current RPS schedule. Case 2 is the base case, where 15.6 MW per month is the historic trailing twelve month (TTM) average build rate in New Jersey. Case 1 represents the bear case, or 75%, of the TTM average build rate. Case 3 represents the bull case, or 150%, of the TTM average build rate.

Figure 1.

In an effort to forestall the cliff, S2276 proposes to once again pull forward demand from future years for the EY2019 – EY2021 energy years as follows: in EY2018, pull forward 52 MWs; in EY2019, 122 MWs; in EY2020, 115 MWs; and in EY2021, 115 MWs. This pull forward would accelerate SREC demand by 62,400 SRECs in EY2018; by 146,400 SRECs in EY 2019; and by 138,000 SRECs in each EY2020 and EY2021. The adjustments will allow for the continued growth of New Jersey’s solar industry, which employs more than 7,100 people across 528 solar companies. To date, New Jersey has installed more than 1.6 GW of solar capacity, which is enough to power 257,000 homes and rank the State 4th in the nation.

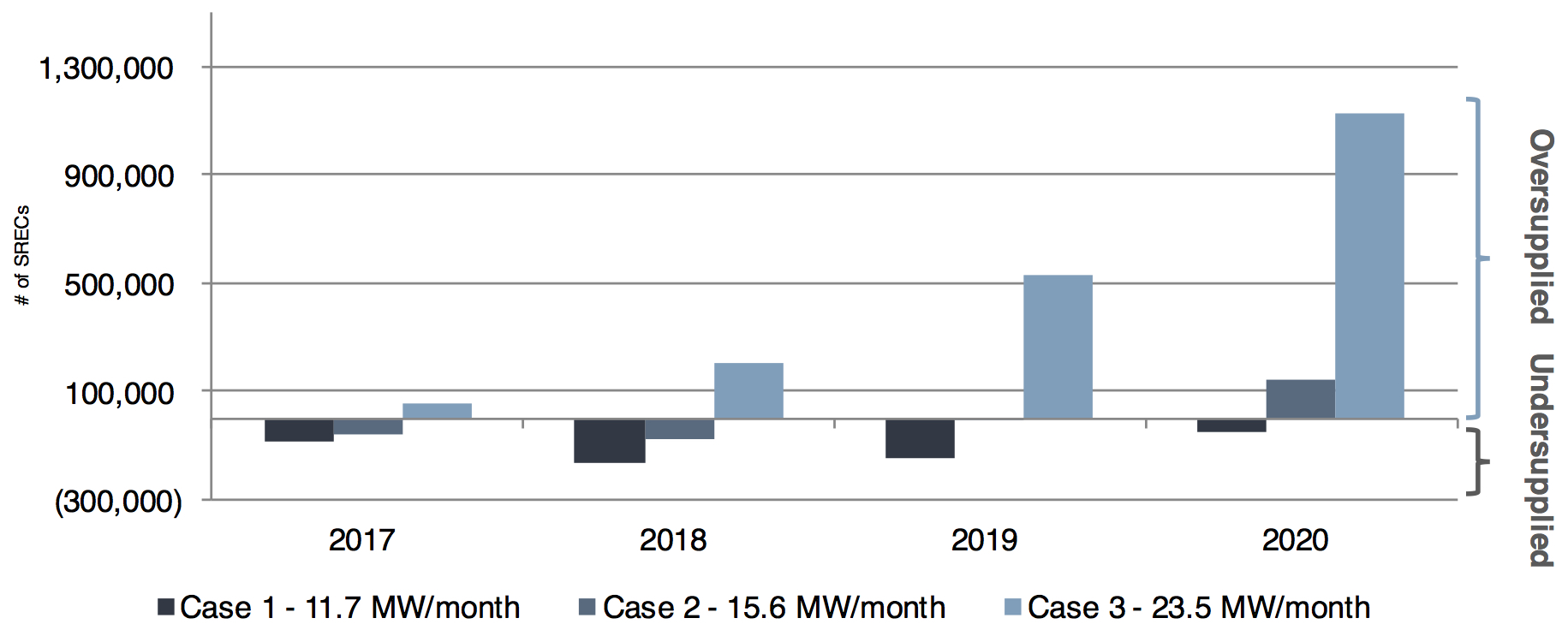

Figure 2 below represents the potential oversupply/undersupply scenarios with the demand pull forward, using the same three potential capacity growth scenarios from Figure 1. The RPS demand figures for 2018, 2019, and 2020 have been adjusted upward by the SREC-equivalent demand increases proposed in S2276.

Figure 2.

In addition to the short-term solution of the pull forward of RPS demand, the bill aims to stimulate the development of long-term solutions through its establishment of the Solar Energy Study Commission. The Commission will be composed of 22 relevant stakeholders, who will provide policymakers with information and best practices for designing and implementing long term solar policies. Under the proposed amended RPS schedule, which ends in June 2021, the Commission would be charged with presenting policymakers with recommendations for New Jersey before the end of the 2021 Energy Year.

S2276 has earned support from members of the New Jersey-based New Jersey Solar Energy Coalition, the New Jersey Solar Grid Supply Association, national and regional members of SEIA and MSEIA, and the IBEW. The bill will be heard at the Senate Environment and Energy Meeting on Monday, June 6.

SRECTrade will continue to track and report on the status of the bill as it progresses this summer.

Disclaimer. This document, data, and/or any of its components (collectively, the “Materials”) are for informational purposes only. The Materials are not intended as investment, tax, legal, or financial advice, or as an offer or solicitation for the purpose or sale of any financial instrument. SRECTrade, Inc. does not warranty or guarantee the market data or other information included herein, as to its completeness, accuracy, or fitness for a particular purpose, express or implied, and such market data and information are subject to change without notice. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Any comments or statements made herein do not necessarily reflect those of SRECTrade, Inc. SRECTrade, Inc. may have issued, and may in the future issue, other communications, data, or reports that are inconsistent with, and reach different conclusions from, the information presented herein.

Copyright. This document is protected by copyright laws and contains material proprietary to SRECTrade, Inc. This document, data, and/or any of its components (collectively, the “Materials”) may not be reproduced, republished, distributed, transmitted, displayed, broadcasted or otherwise disseminated or exploited in any manner without the express prior written permission of SRECTrade, Inc. The receipt or possession of the Materials does not convey any rights to reproduce, disclose, or distribute its contents, or to manufacture, use, or sell anything that it may describe, in whole or in part. If consent to use the Materials is granted, reference and sourcing must be attributed to the Materials and to SRECTrade, Inc. If you have questions about the use or reproduction of the Materials, please contact SRECTrade, Inc.