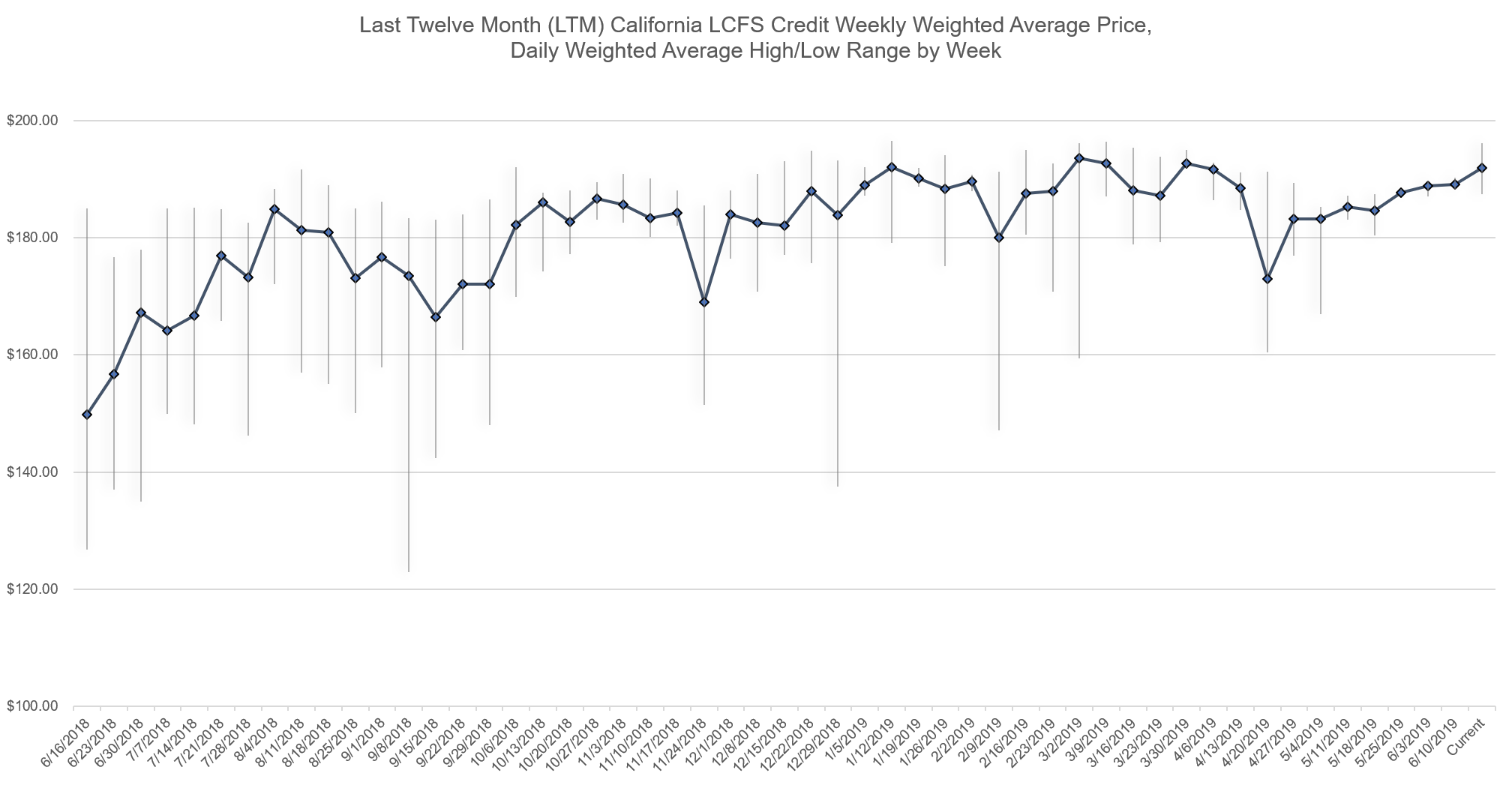

As per data released by the California Air Resources Board (CARB) on June 25th, the Low Carbon Fuel Standard (LCFS) market continued its upward price trend this past week, increasing to a weighted average weekly price of $191.87. This is up $2.75 from last week’s average price of $189.12 and the fourth straight week we have seen an uptick in LCFS pricing. This is also the first time since early April that the market saw pricing above $190 per credit. The market, however, did see a significant decrease in volume this past week with 39,827 credits transferred, down from last week’s volume of 86,403 and the last twelve month (LTM) weekly average of 237,742.

Please click on the pricing chart below for a visualization of LTM trends.

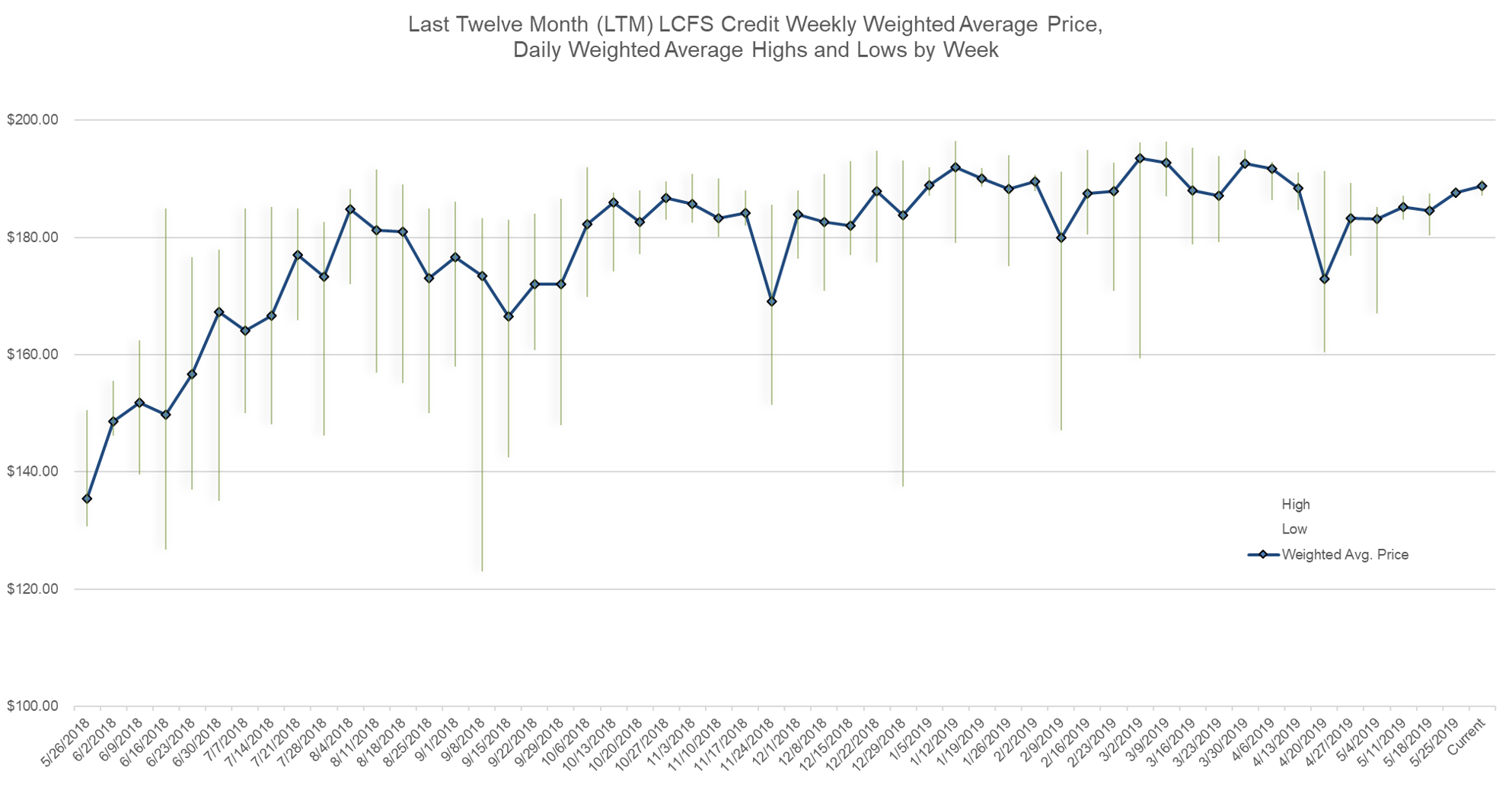

As per data released by the California Air Resources Board (CARB) on June 18th, the Low Carbon Fuel Standard (LCFS) market continued its upward price trend this past week, increasing to a weighted average weekly price of $189.12. This is up $0.28 from last week’s average price of $188.84 and the third straight week we have seen an uptick in LCFS pricing. The market saw a decrease in volume this past week with 86,403 credits transferred, down from last week’s volume of 325,708 and the last twelve month (LTM) weekly average of 241,706.

Please click on the pricing chart below for a visualization of LTM trends.

Source: California Air Resources Board (CARB)Tweet

As per data released by the California Air Resources Board (CARB) on June 11th, the Low Carbon Fuel Standard (LCFS) market continued its upward price trend this past week, increasing to a weighted average weekly price of $188.84. This is up $1.78 from last week’s average price of $187.06 and the second straight week we have seen an uptick in LCFS pricing. The market also saw a jump in volume this past week with 325,708 credits transferred, up from last week’s volume of 106,031 and the last twelve month (LTM) weekly average of 243,077.

In recent weeks, we have also seen a decrease in daily price variance over a given week. This indicates a more uniformly priced market and perhaps a steadier volume of credits transacted on a daily basis.

Please click on the pricing chart below for a visualization of LTM trends.

Data Source: California Air Resources Board (CARB)Tweet

On June 13th, Yaniv Lewis, an Environmental Markets Associate at SRECTrade, is speaking at a Voice of the Customer Event hosted by CALSTART, a non-profit in the clean transportation industry. The event, which will be a discussion on Medium and Heavy-Duty Electric Step Vans, will take place at the Clovis Veterans Memorial District in Clovis, CA from 10:00 AM – 2:00 PM.

Yaniv will speak on the Low Carbon Fuel Standard (LCFS) market, a state incentive that encourages the uptake of low carbon intensive vehicles. SRECTrade provides its services to participants across the LCFS market, providing credit portfolio management and brokerage services to clean fuel asset owners and credit generators.

Learn more about the event here and register for free here.

On May 22nd, 2019, Maryland Governor Larry Hogan announced his decision to let the Maryland Clean Energy Jobs Act pass without his signature. The Act increases Maryland’s Renewable Portfolio Standard to an aggressive 50% by 2030. Additionally, the solar carve out target increased to 14.5% by 2028 and the Solar Alternative Compliance Penalty (SACP) was adjusted to $100.00 in 2019 and 2020, and decreasing each year thereafter. In response to these anticipated, and now enacted, legislative changes, the SREC market in Maryland has experienced a significant upward swing from $11.00 to $65.00 since the beginning of 2019.

Electricity load that was signed under contract prior to the bill’s effective date of October 1, 2019, is not subject to the new compliance obligations. Our calculations assume that approximately 80% of the 2019 electricity load is under prior contract and therefore exempt, with 25% of that exempt load rolling into the new compliance obligations each year moving forward.

Solar build rates have been trending downwards over the last six months in comparison to the last twelve months. Assuming no drastic decrease in build rate, we expect the market to be oversupplied in 2019, and undersupplied each year thereafter. The enclosed analysis further details the implications of the Maryland Clean Energy Jobs Act and the potential responses from the MD SREC market.

SRECTrade is excited to announce its new HelioScope integration, allowing users to seamlessly transfer data between the online platforms. This new feature provides SRECTrade applicants with the ability to import project details from HelioScope to prefill fields in the SRECTrade project application. The integration will save time for SRECTrade’s partners and reduce the chance of error during the renewable energy credit (REC) application process.

To import HelioScope project details, a HelioScope user needs to obtain an API Token and connect it with their SRECTrade account. This will allow the user to utilize the information stored in HelioScope to populate REC application fields such as facility type, owner details, array setup, and more. For more specific instructions on how to utilize the HelioScope integration, please email installers@srectrade.com.

The HelioScope integration is the latest chapter in SRECTrade’s history of REC management and transaction innovation. Other recent technology advancements by SRECTrade include partnerships with eGauge and Fronius to allow solar owners using these inverter and meter products to automatically report their production to PJM-GATS, the REC tracking registry for much of the Midwest and Mid-Atlantic.

SRECTrade is always working toward automating the onboarding and management of assets in environmental commodity markets. For more information on technology integrations and partnerships, please reach out to clientservices@srectrade.com.

A copy of the full press release can be found here.

The Davis-Basse Nuclear Power Station will be subsidized under Ohio House Bill 6. Source: News-Herald

On Wednesday, May 29th, the Ohio House of Representatives passed House Bill 6 (HB 6) 53-43 that would repeal the state’s renewable energy mandate and replace it with a nuclear subsidy program under the moniker “Clean Air Program”. This nuclear subsidy program would help bailout two ailing nuclear power plants in Ohio owned by bankrupt utility FirstEnergy Solutions by adding a $1 surcharge on customers’ monthly utility bills. The program would also extend a surcharge of $2.50 per month through 2030 to support ailing coal plants across the state.

The bill would eliminate the renewable portfolio standard (RPS) in Ohio, a key component to maintaining the financial viability of renewables compared with other fossil-fuel based electricity generation resources. As such, nearly all renewable assets generating OH-certified renewable energy credit (REC) or solar renewable energy credit (SREC) products would cease to generate these credits as of the effective date of the bill. Additionally, the bill would do away with the nearly $200 million program to fund energy efficiency and demand response initiatives, which saved Ohio customers over $5 billion from 2009 to 2017, according to the Midwest Energy Efficiency Alliance.

The bill now moves on to the Ohio Senate. While state senators have not publicly voiced their support of the bill, outspoken support from Governor Mike DeWine and the Republican majority in the senate gives the bill momentum to pass.

SRECTrade strongly urges constituents and market stakeholders to reach out to members of the Ohio State Senate and voice their concern with this Bill. The Senate directory can be found here. SRECTrade will continue monitoring these policy proceedings closely and provide updates.

On Friday, May 22nd, Governor Larry Hogan announced that he would let the Maryland Clean Energy Jobs Act (SB-516) pass without his signature. The Governor’s decision to let the bill pass puts Maryland at the forefront of a growing list of states with aggressive renewable targets. This legislation requires 50% of Maryland’s energy to come from renewable sources and 14.5% from in-state solar, by 2030. In addition to the 2030 targets, the bill mandates that the state conduct research on strategies to reach 100% renewable energy sources by 2040, among other initiatives.

The Governor supplemented his decision to let the bill pass unsigned with a letter to Maryland Senate President, Thomas V. Miller, expressing his concerns with the bill and affirming his promise to continue pushing for a cleaner portfolio of energy resources in Maryland. SRECTrade will conduct further analysis on the impacts of this legislation and publish a comprehensive SREC market analysis in the coming weeks.

On April 30th, the California Air Resources Board (CARB) released Q4 2018 data on the Low Carbon Fuel Standard (LCFS) market in California. Notably, the market saw an LCFS credit surplus of approximately 67k credits, snapping a deficit streak of four straight quarters. Approximately 3.27 million metric tons (MT) of credits were generated in Q4 2018 compared to 3.20 million MT of deficits in the same time frame. This credit surplus can be largely attributed to the uptick in clean diesel substitutes, namely renewable diesel and bio-diesel, which from a volumetric perspective, increased 37.2% and 14.8%, respectively, from Q3 to Q4 2018.

The following chart shows credit production changes for the highest credit-producing fuels in the LCFS market:

Source: CARB

With an average quarter-over-quarter credit increase rate of 9.11% since Q1 2011, the Q4 2018 increase of 16.89% from Q3 2018 is well above the running average. However, when factoring out the increases in renewable diesel and bio-diesel credit generation, overall credit generation only increased 1.45% from Q3 to Q4 2018. As such, monitoring the influx of renewable diesel and bio-diesel in the marketplace will be integral to projecting credit growth over the next few quarters.

The following chart shows deficit changes for the two baseline deficit-producing fuels in the LCFS market:

Source: CARB

While CARBOB and diesel fuels both saw a volumetric and deficit-production decline in Q4 2018, the influx of renewable diesel into the market produced 160k deficits in Q4 2018. This outpaced the deficit decrease in traditional deficit-producing fuels, increasing the overall deficit count by 2.03% from Q3 2018.

The following chart released by CARB illustrates the overall LCFS market trends:

Source: CARB

With a step down in the Carbon Intensity (CI) Compliance Standard in 2019, we will likely see an uptick in deficit production beginning in Q1 2019, barring any major changes in fuel production. The influx of renewable diesel will continue to be a determining market force from both a credit and deficit perspective.

With regards to pricing, in recent weeks, we have seen pricing come off its ~$200 peak after CARB proposed a hard $200 price cap (in 2016 $ indexed for inflation) on the program in a workshop on April 5th. As of recent, CA LCFS spot market pricing has ranged between $180 and $185/credit.

SRECTrade offers LCFS credit management and brokerage services to electric vehicle (EV) fleet operators, OEMs, EV charging station owners, and other asset owners. We help our clients navigate through the entire LCFS process including asset registration, ongoing reporting requirements, transacting, settlement, and remittance of funds. Our domain expertise in environmental commodity markets allows us to provide our clients with industry leading regulatory and market knowledge. Please reach out to cleanfuels@srectrade.com for more information.

On Monday, April 29th, Pennsylvania Governor Tom Wolf declared his support for Senate Bill 600 (SB 600). In conjunction, Gov. Wolf released the fourth iteration of the state’s Climate Action Plan, providing recommendations for how the state can mitigate climate change, and also announced that Pennsylvania joined the U.S. Climate Alliance, a bipartisan coalition of 24 states committed to reducing greenhouse gas emissions.

Initially introduced in the Pennsylvania General Assembly on April 10th, SB 600 was referred to the Consumer Protection and Professional Licensure Committee on April 29th. The bill updates the state’s Alternative Energy Portfolio Standards (AEPS) for the first time since the AEPS was established in 2004, calling for four primary changes:

Expand the AEPS Tier I requirement from 8% by 2021 to 30% by 2030

Expand the AEPS solar carve-out from 0.5% by 2021 to 10% by 2030, including 7.5% for grid-supply solar and 2.5% for distributed generation (DG) solar

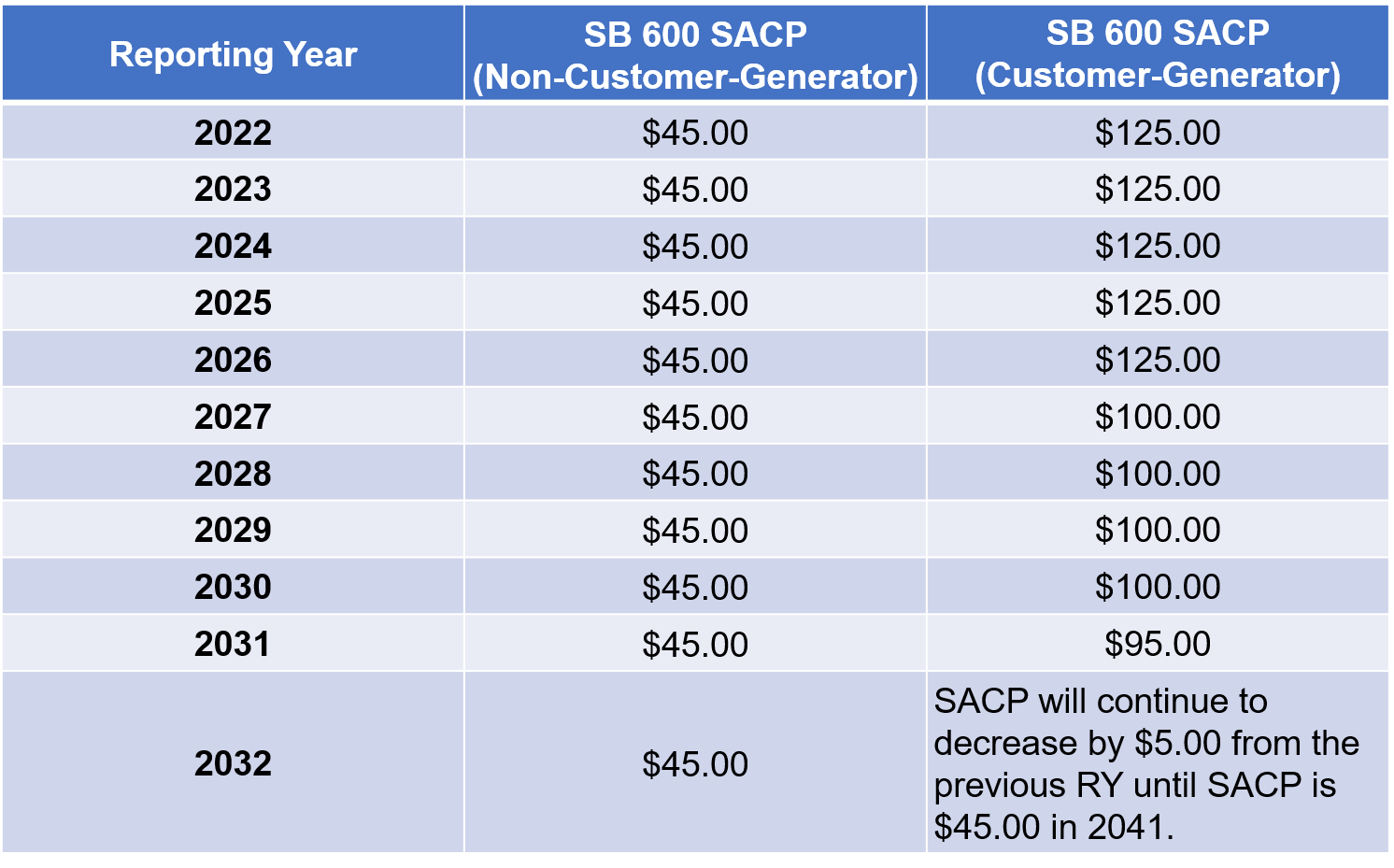

Minimize rate increases for electricity customers by introducing fixed alternative compliance payment (ACP) schedules and a 15-year SREC eligibility term for solar facilities (beginning on June 1, 2021)

Direct the PA Public Utilities Commission (PUC) to explore a program for renewable energy storage

Table 1.Table 2.Table 3.

SB 600’s introduction of solar carve-out compliance categories between “customer-generators” and “non-customer-generators” marks a first for the state. Tables 2 and 3 above display the proposed solar carve-out requirements and solar alternative compliance payment (SACP) schedules between the two respective categories. The bill defines customer-generators as solar facilities that were certified on or before May 31, 2021 and also appears to define them as “behind-the-meter” facilities. Conversely, it appears that non-customer-generators are defined as grid-supply facilities, although the exact definitions of both categories may be subject to change.