The NJ SREC market has been active this week as traders gear up for tomorrow’s start to the annual BGS auction. In the auction, electricity providers will be awarded parcels of load to be served across the state by the four major Electric Distribution Companies (EDCs) – Public Service Electric & Gas (PSE&G), Atlantic City Electric Company (ACE), Jersey Central Power & Light (JCP&L), and Rockland Electric Company (RECO) – between 2017 and 2019. As wholesale power providers find out their future obligation for electricity production, they also begin to hedge their forward exposure to the RPS SREC obligation. This auction has traditionally been the single biggest liquidity event of the year for the NJ SREC market so we believe this to be a timely opportunity to update our capacity models.

Our New Jersey SREC Update presentation can be found here.

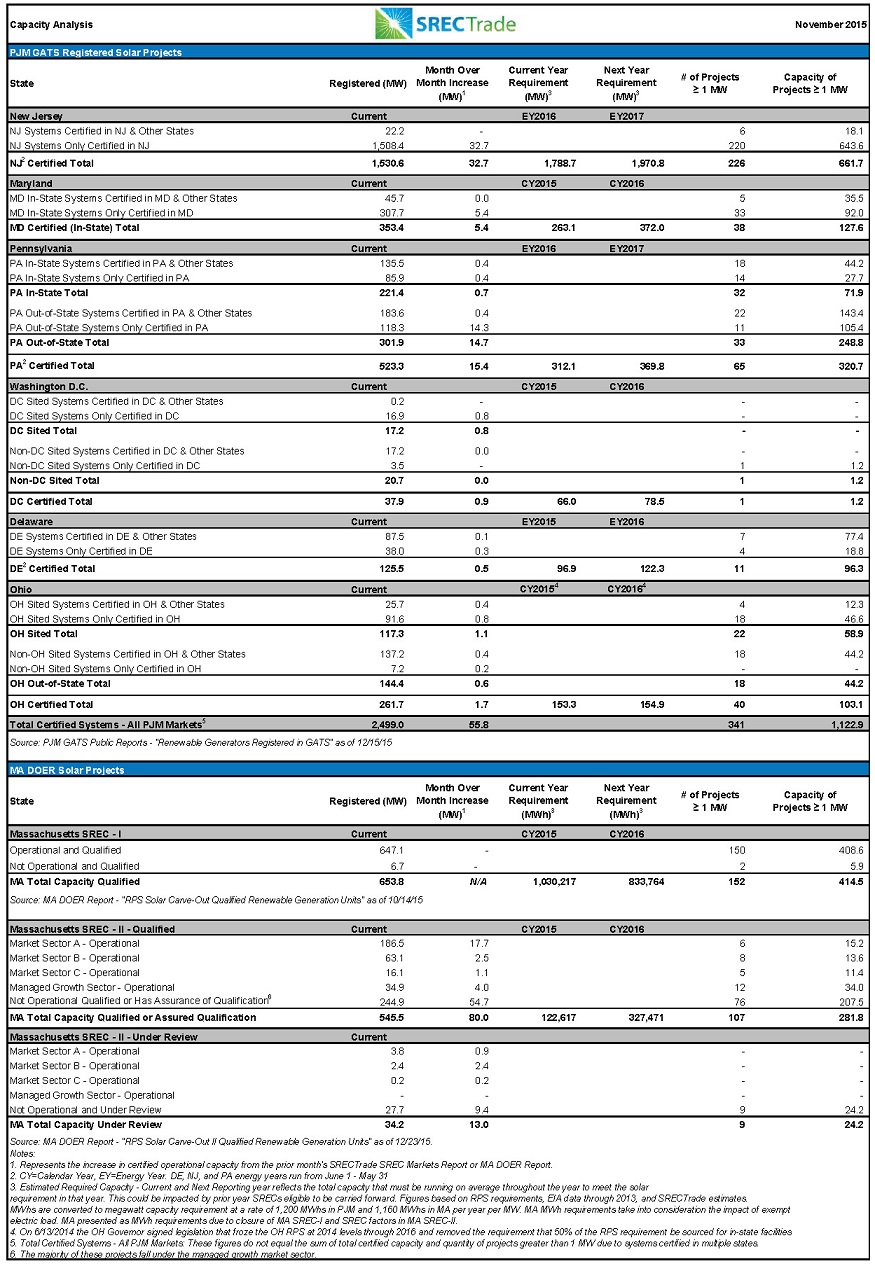

The trend in build rate has kept largely in line with our October 2015 update, when we emphasized that the market is projected to be fundamentally balanced on average through 2018, with the maximum range of 10.6% undersupply to 7.3% oversupply. The trend in 2019 and beyond, however, begins to turn towards oversupply in 2019 and 2020 as the RPS percentage growth slows. In the medium term we expect to see NJ SREC markets trade largely in line with the average price range witnessed in spot vintages. In the short term, however, the renewed source of demand from compliance buyers shifting their focus to 2017 and 2018 obligations should be extremely supportive for prices.

One final observation pertains to the potential impact that a steadily more risk-averse attitude towards credit exposure could have on the ability for members of the solar industry to access liquidity in both OTC and electronic SREC markets. As many firm’s credit requirements become more stringent, we have noticed a delineation in the market where the price that is being traded between two investment-grade (IG) counterparties is growing further and further away from the levels that are accessible to non-IG solar developers and asset owners.

As always, this document is informational in purpose to assist in explaining the focus on NJ Solar RECs over the coming weeks.

Disclaimer. This document, data, and/or any of its components (collectively, the “Materials”) are for informational purposes only. The Materials are not intended as investment, tax, legal, or financial advice, or as an offer or solicitation for the purpose or sale of any financial instrument. SRECTrade, Inc. does not warranty or guarantee the market data or other information included herein, as to its completeness, accuracy, or fitness for a particular purpose, express or implied, and such market data and information are subject to change without notice. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Any comments or statements made herein do not necessarily reflect those of SRECTrade, Inc. SRECTrade, Inc. may have issued, and may in the future issue, other communications, data, or reports that are inconsistent with, and reach different conclusions from, the information presented herein.

Copyright. This document is protected by copyright laws and contains material proprietary toSRECTrade, Inc. This document, data, and/or any of its components (collectively, the “Materials”) may not be reproduced, republished, distributed, transmitted, displayed, broadcasted or otherwise disseminated or exploited in any manner without the express prior written permission ofSRECTrade, Inc. The receipt or possession of the Materials does not convey any rights to reproduce, disclose, or distribute its contents, or to manufacture, use, or sell anything that it may describe, in whole or in part. If consent to use the Materials is granted, reference and sourcing must be attributed to the Materials and to SRECTrade, Inc. If you have questions about the use or reproduction of the Materials, please contact SRECTrade, Inc.

Tweet