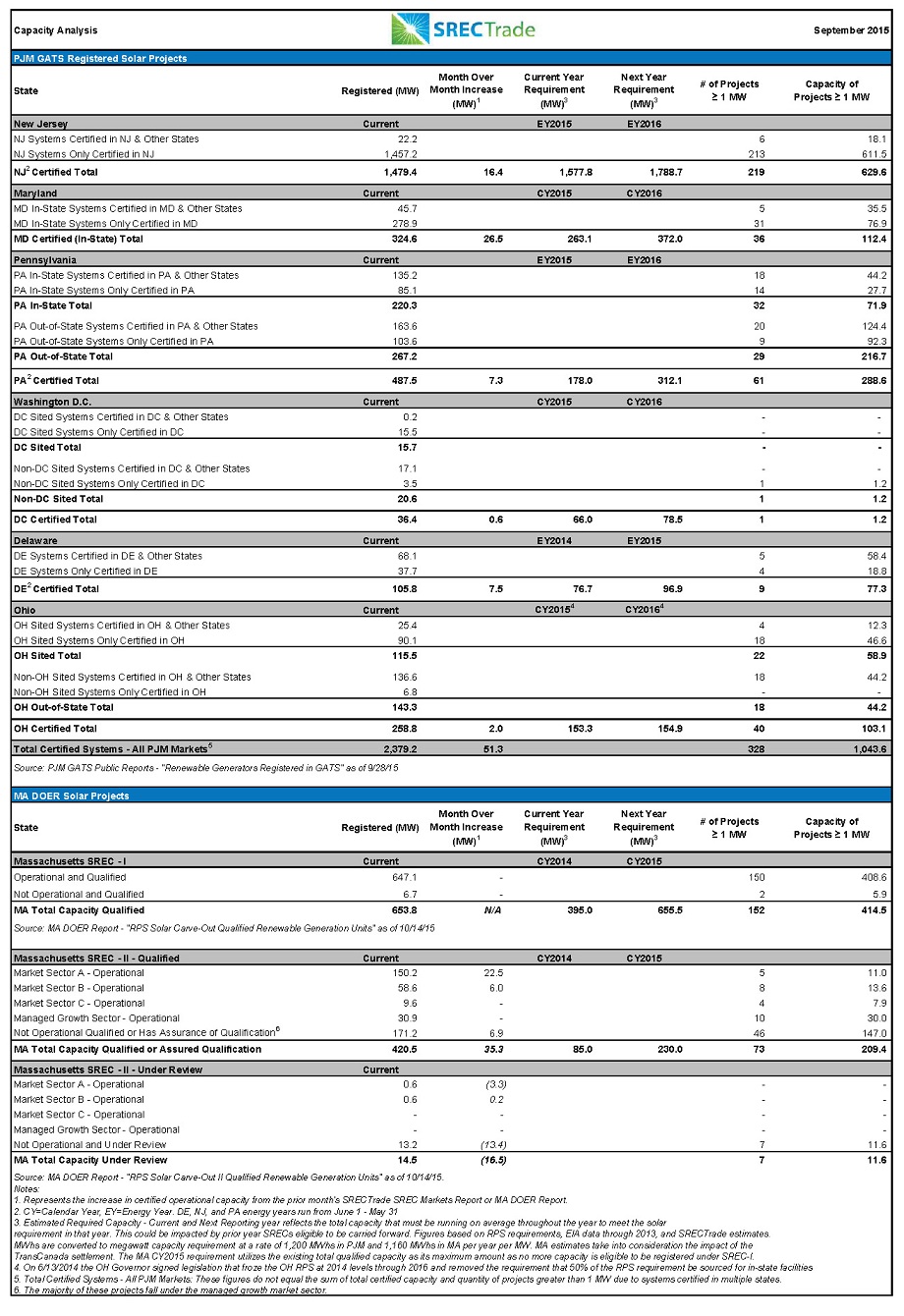

Last week, attention focused on the Maryland SREC market. On Monday, 10/19/15, Maryland regulated utilities awarded load auction bids for electricity supply. Electric load was contracted for anywhere between 3 and 24 months into the future. Once load suppliers begin to lock in their load obligations, attention naturally turns to the REC markets to begin planning for the corresponding compliance obligations.

Given the additional attention on the recent load auction and the consequent trading activity in the MD SREC market, we have refreshed our capacity scenarios to get a stronger sense of the current balance between supply from recently built projects and demand from RPS compliance obligations.

Our most recent MD SREC capacity presentation can be found here.

As of our last MD capacity update, Last Twelve Month (LTM) monthly build rates were 5.8 MW per month. Due to a remaining balance of approximately 73,400 CY 2013 and 2014 SRECs and a strong Q4 2014 build, the market was expected to be slightly oversupplied in the short term (2015 and 2016) by about 10%-30%; depending on forecast monthly solar build rates. Despite this short term oversupply, the market was projected to return to balance by 2017 with significant under supply in 2018 and 2019. At the time, supply/demand balance and observed build rates justified the thesis that the MD solar market had the ability to digest more project build.

Since the late spring / early summer, the PJM GATS renewable generators report shows Maryland experienced a strong uptick in new build during the summer, with build rates from June through August increasing 34% from the previous three months ending in May.

Average LTM build rates now stand at 10.6 MW per month. At this increased pace, the Maryland SREC market will experience over supply in the coming years. Across three scenarios – 75%, 100%, and 150% of LTM solar build rates – the market is forecast to be oversupplied through 2019.

What this means for MD SREC pricing

If these observed build rates continue into the future, downward pricing pressure will result as more and more supply is brought to market. This is particularly relevant now, as electricity companies who have sold electric supply for the next 24 months will be looking to buy their SREC exposure for a similar time period. Market participants can look at forward structures such as multi-year SREC strips as an opportunity to lock in forward pricing to protect from any future price movement.

As always, this analysis is informational only in purpose in order to help explain the emphasis on MD SREC markets last week. We will continue to watch the markets closely and stay on top of new MD capacity data as it is updated by PJM-GATS.

Disclaimer. This document, data, and/or any of its components (collectively, the “Materials”) are for informational purposes only. The Materials are not intended as investment, tax, legal, or financial advice, or as an offer or solicitation for the purpose or sale of any financial instrument. SRECTrade, Inc. does not warranty or guarantee the market data or other information included herein, as to its completeness, accuracy, or fitness for a particular purpose, express or implied, and such market data and information are subject to change without notice. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Any comments or statements made herein do not necessarily reflect those of SRECTrade, Inc. SRECTrade, Inc. may have issued, and may in the future issue, other communications, data, or reports that are inconsistent with, and reach different conclusions from, the information presented herein.

Copyright. This document is protected by copyright laws and contains material proprietary to SRECTrade, Inc. This document, data, and/or any of its components (collectively, the “Materials”) may not be reproduced, republished, distributed, transmitted, displayed, broadcasted or otherwise disseminated or exploited in any manner without the express prior written permission of SRECTrade, Inc. The receipt or possession of the Materials does not convey any rights to reproduce, disclose, or distribute its contents, or to manufacture, use, or sell anything that it may describe, in whole or in part. If consent to use the Materials is granted, reference and sourcing must be attributed to the Materials and to SRECTrade, Inc. If you have questions about the use or reproduction of the Materials, please contact SRECTrade, Inc.