On December 19, the California Air Resources Board (CARB) revealed their long-awaited proposal to update and extend the Low Carbon Fuel Standard (LCFS). Among the most significant changes:

Increases 2030 carbon intensity (CI) targets from 20% to 30%, including a one-time 5% reduction of the CI benchmark in 2025

Extends CI reduction targets to 90% CI by 2045

Creates new auto-acceleration mechanism to help stabilize the credit market in the event of rapid decarbonization that outpaces deficits, beginning in 2028

Phases in some limitations to biomethane crediting

Reduces credits from eForklifts

Adds third-party verification requirement to electricity and other fuels

Expands ZEV infrastructure crediting for medium and heavy-duty charging

Staff published a Preliminary Draft Report, Regulatory Text, and nearly 12 total documents on its rulemaking page. These 500+ pages make for a good read over the holiday break.

What to Watch for Next

The agency indicated a formal regulatory notice will be issued in early January 2024, which kicks off a 45-day public comment period. The proposed regulations can then be adopted at a subsequent board meeting, potentially as early as March 21.

Check back here for more analysis on these proposed changes!

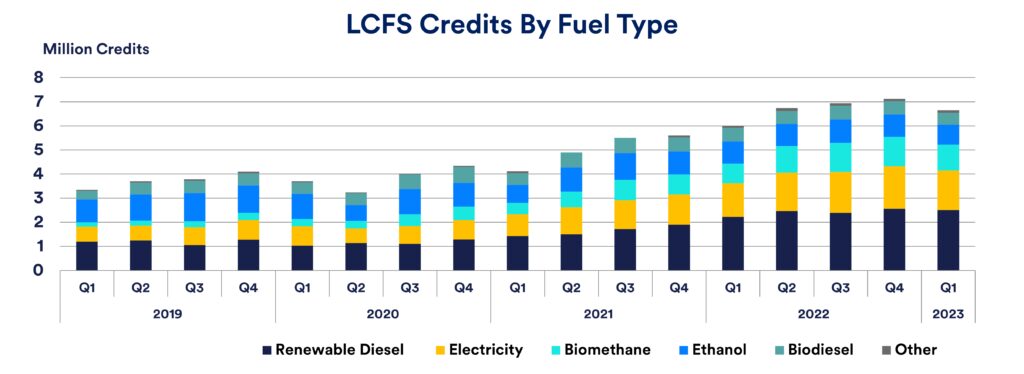

The California Air Resources Board (CARB) published Q2 2023 data for the Low Carbon Fuel Standard (LCFS) today. Consistent with trends dating back to 2021, low carbon fuel producers generated 1.6M more credits than deficits, pushing the cumulative credit bank to over 18M credits.

Source: California Air Resources Board

Record Credit Generation

More credits were generated in Q2 (5.5M) than in any previous quarter of the program, led by increases from the largest credit sources: renewable diesel (14%), renewable natural gas (28%), and electricity (7%). Two key trends underpin the consistent growth in net credits: 54% of diesel sold in CA last quarter came from renewable feedstocks while the average carbon intensity (CI) of renewable natural gas fell to its lowest mark of -131 g/MJ.

There was also a 50% increase in credits from alternative jet fuel (also referred to as sustainable aviation fuel) which still represents less than 1% of all credits. Meanwhile, there were modest declines in credits from ethanol (-11%), propane (-11%), and biodiesel (-5%).

Source: California Air Resources Board

EV Credits Rebound

Credits from EV charging bounced back from a quarterly decline in Q1, driven by increases in both light-duty (12%) and heavy-duty (11%) on-road EV charging. Residential EV charging still made up about half of all EV credits, ahead of forklifts (23%) and on-road EVs (18%). Credits from DC fast-charging infrastructure rose by about 12%. Overall, EVs are the second largest source of credits, representing about one-quarter of all credits in the program.

Source: California Air Resources Board

Credit Prices Hover Above Six-Month Low

LCFS credit prices closed October around $68/credit, up slightly from six-month lows in September following CARB’s publication of a regulatory document which hinted at major program changes including the strengthening of CI targets and limitations on biomethane crediting. CARB is expected to publish its final proposal by December, which triggers a 45-day public comment period before the governing board can approve rule changes.

The first batch of data for the new Washington Clean Fuels Standard (CFS) has been made available by the Washington State Department of Ecology. So far, Ecology has published:

No credits were transferred in July after technical issues with the Washington Fuel Reporting Systems triggered a one-month delay in the first issuance of credits. However, 27,055 credits were transferred in August. The average price from the four reported trades was $106.66. The price of Washington CFS credits was about midway between those reported in CA ($77) and OR ($137) during the same month. Credits from one program cannot be sold in another.

Q1 2023 Credit and Deficits

Ecology reported 275k credits generated and 227k deficits generated, a net credit build of about 47k credits. Entities with compliance obligations do not have to retire credits until next year, and credits do not expire so they may be held indefinitely by market participants.

The largest source of credits was ethanol (75%), followed by renewable diesel (12.1%), biodiesel (11.8%), and electricity (10.8%). Credits from residential EV charging, which are separately calculated and issued by Ecology, have not yet been issued for Q1 or Q2.

The deadline for reporting fuel consumption for the Q2 2023 reporting period is today. Ecology has not yet set a publication schedule for reporting quarterly credit and deficit data.

Source: Washington Department of Ecology

What’s Next for the Washington CFS?

Ecology will create a zero-emission vehicle infrastructure or “capacity credit” program for public DC fast-charging and hydrogen refueling stations. Stations approved under this program may generate CFS credits based on the fueling capacity of those stations. Guidance on this program is expected to be released before the end of the year.

Ecology must also address the inclusion of alternative jet fuel pathways in the CFS after the passage of SB 5447. A rulemaking may be initiated as soon as this year or early next year.

The timeline for implementing changes to the California Low Carbon Fuel Standard (LCFS) became clearer last week. At an industry conference, California Air Resources Board (CARB) Executive Director Dr. Steven Cliff indicated a final proposal would be made available in the “November timeframe” with hopes of approval by next spring. The announcement came after the September 8 publication of the Standardized Regulatory Impact Assessment (SRIA).

Under this timeline. CARB could implement a mid-year adjustment to the 2024 carbon intensity targets, increasing compliance obligations for fuel suppliers. An even more significant adjustment or “step down” is being considered for the 2025 targets, as indicated in the SRIA. The document evaluated other significant changes to the program, including a target acceleration mechanism, the inclusion of intrastate fossil jet fuel as a regulated fuel, and the phasing out of biomethane and forklift crediting. However, Dr. Cliff reiterated that the SRIA, which precedes any formal rule-changes to be considered by the regulatory body which oversees the LCFS, “is not the final proposal. It’s not even the proposal.”

Source: CARB Standardized Regulatory Impact Assessment for LCFS 2023 Amendments

What To Watch For Next

Regulatory staff will present on changes to the LCFS at the September 28 CARB non-voting meeting. The next formal milestone will be the publication of a Rulemaking Package which starts the 45-day public comment period, after which CARB may adopt new provisions to the LCFS rules.

Source: CARB Staff Presentation at 9/14 EJAC Committee Tweet

The California Air Resources Board (CARB) held a workshop on August 16 to present updates to a model that assesses the feasibility and economic impact of proposed changes to the Low Carbon Fuel Standard (LCFS). Although the workshop did not specifically address policy changes, the inputs of this model are suggestive of what CARB may put forward in formal rule changes coming later this fall.

Why is CARB making changes to the LCFS?

The last time significant changes to the LCFS were made was in 2018. Since then, the agency has workshopped several policy and procedural changes and received significant stakeholder and community feedback. During workshops held last summer, CARB presented a plan to align LCFS with several key climate policies, most notably the 2022 Scoping Plan, which was formally adopted in December 2022.

Key Program Changes

The model inputs included many of the policy changes that have been discussed at public workshops over the past 18 months and may hint at what the agency will propose later this year. Some of these changes are highlighted below:

Accelerating Carbon Intensity Targets

Carbon intensity, a measure of lifecycle emissions of a fuel, is used as a benchmark to compare gasoline, diesel, and other low carbon fuels such as biofuels and electricity. The benchmark decreases each year to meet the current target of 20% reduction from 2010 levels by 2020. As the benchmark decreases, conventional gasoline and diesel generate more deficits (i.e. greater demand for credits) which produces the long-term incentive for lower carbon fuels.

Reduction in CI Benchmark Over Time

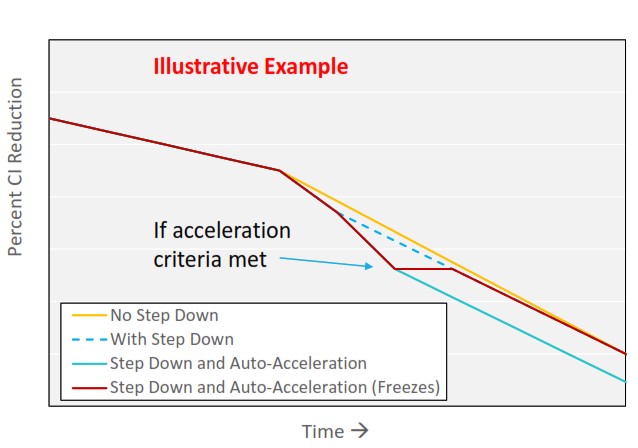

CARB has proposed advancing the 2030 target to between 25% and 35% reduction, while adding a 2045 target of 90% reduction. The 2030 acceleration is significant because it would increase the demand for credits in the near term, depending in part on how the targets “step down” from their current levels in order to meet the new 2030 target. Proponents of steeper 2030 targets argue this will provide needed price support for the LCFS credit market which has significantly declined in recent years due largely to an oversupply in credits. Others caution that overly stringent targets would increase fuel prices and could undermine political support for the program.

In the latest iteration of the model, CARB included a 30% reduction target for 2030 with a significant step down between 2024 and 2025. While not an official proposal from CARB, it might indicate what the agency is ready to move forward with in the fall.

CI Adjustment Mechanisms

Source: California Air Resources Board

Phasing Out eForklifts

In previous workshops, CARB has proposed reducing and eventually phasing out credit generation from eForklifts. Staff discussed reducing the credit generation potential of lighter classes of forklifts and requiring electricity consumption to be metered. Forklifts are unique in that CARB allows for electricity consumption to be estimated. However, both the Oregon Clean Fuels Program and the Washington Clean Fuel Standard have recently required metering for electric forklifts in their programs. CARB’s latest model included a significant reduction in credits from forklifts, suggesting these changes are still on the table.

Verification Requirements for ElectricityCredits

In a previous workshop, CARB proposed requiring all participants generating credits from electric vehicles to go through an annual verification process. Electricity is the only major credit source where fuel consumption reporting is not required to be independently verified. Other programs, such as the Canadian Clean Fuel Regulations require verification for all fuel types.

Expanding Infrastructure Crediting to Medium/Heavy-Duty Vehicle Charging

Under the LCFS, some public fast-charging stations are eligible to generate credits based on the total capacity of the site, not solely on electricity consumption. CARB has proposed expanding these provisions to stations that provide charging to multiple medium and heavy-duty fleets. CARB’s latest model included credit generation from this pathway, suggesting that the agency is still considering this change.

What’s Next for LCFS?

During the workshop, staff shared an updated timeline which confirmed that formal changes to LCFS will not be considered for adoption until early 2024. However, the agency expects to move forward with the formal rulemaking process later this fall, and implement the changes “sometime in 2024.”

The California Air Resources Board (CARB) published quarterly program data for the Low Carbon Fuel Standard (LCFS) on June 30, 2023 and announced another workshop for August 16 to discuss changes to the program.

Credit Bank Adds 1.3M Net Credits After Sluggish Q1

The cumulative credit bank, a measure of net credit generation over the lifetime of the program, grew for an eighth consecutive quarter and now stands at 16.5M credits. Deficits were down in Q1 (-3%), driven largely by a decline in gasoline volume (-9%). Credits from all sources (-6%) fell for the first time in 2 years driven in part by reductions in volume from electricity (-5%), biodiesel (-3%), and ethanol (-2%). Average carbon intensities (CI) were up across the major credit sources as well, including RNG (+21%), biodiesel (+8%), RD (+9%), and electricity (+3%). Finally, the more stringent CI targets for 2023 kicked in, which reduces the number of credits per unit of low carbon fuel when compared to 2022.

EV Credits Take a Step Back in Q1

Credits from electricity fell last quarter (-7%) for the first time since the COVID pandemic, driven primarily by a 12% decline in residential EV charging credits which are issued to utilities based on a formula. Credits also decreased across other categories including eForklifts (-1%), ocean-going vessels (-13%) and fixed-guideways (-11%). EVs still remain the second largest source of credits under the LCFS and among the fastest growing fuel type.

What’s Next for CA LCFS?

CARB scheduled a workshop on August 16 to present updates to their model that is used to assess the feasibility and economic impact of proposed changes to the program, including establishing more stringent 2030 CI targets. In the previous workshop held in May, CARB staff had reiterated their intent to initiate a formal rulemaking process to make changes to the LCFS by this summer, with a targeted implementation date of January 1, 2024.

CARB will release Q2 2023 program data by October 31, 2023.

The California Air Resources Board (CARB) published quarterly program data for the Low Carbon Fuel Standard (LCFS) on April 28, 2023. In this piece, we will provide some analysis of the new data and highlight interesting trends.

Credit Bank Growth Slows

The cumulative credit bank, a measure of net credit generation over the lifetime of the program, grew for a seventh consecutive quarter to reach a new program high of about 15M MT. However, quarter-over-quarter credit growth slowed to 2% while deficits rose by 5%, resulting in a net build of 1.65M MT, slightly lower than last quarter’s build of 1.76M MT and halting a three-quarter trend of growing credit builds.

Source: CARB

Q4 2022 Credit Trends

Renewable diesel (RD) rebounded from a rare quarterly decline in Q3, growing by 7% to a new program high of 2.5M MT. RD remains the largest source of credits under the program at 36%.

Renewable natural gas (RNG) volumes dropped by about 2% but remains the lowest average carbon intensity (CI) fuel at -119 gCO2e/MJ. Notably, a bill was introduced that would direct CARB to restrict dairy digesters from generating credits under the California program.

Credits from ethanol declined by 5%, while credits from biodiesel and hydrogen both dropped by 4%.

Source: CARB

EV Credit Growth Also Slows

Credits from electric vehicles represented one-quarter of all credits under the program but grew by only 66k MT last quarter, the least since Q4 2021. The distribution of credits across the categories of eligible EVs remains unchanged: residential (49%), eForklifts (23%), and non-residential light/medium-duty (15%). Notably, credits from heavy-duty EVs grew by 10% while credits from electric cargo handling equipment and electric refrigeration units both fell by about 5%.

The California Air Resources Board (CARB) published quarterly program data for the Low Carbon Fuel Standard (LCFS) on January 31, 2023. In this piece, we will provide some analysis of the new data and highlight interesting trends.

But First: What is the Credit Bank and Why is it Growing?

Each quarter, CARB issues credits and deficits based on the carbon intensity (CI) and volume of fuel reporting under the program. The cumulative credit bank, a measure of net credit generation over the lifetime of the program, is often used as a proxy for credit supply and demand. This credit bank grew for the first few years of the program, reaching about 10M MT by the end of 2016. From 2017 through the first half of 2021, the credit bank remained largely stable as quarterly net gains were balanced by quarterly net reductions. However, the credit bank has increased significantly since then, reaching about 13.5M MT according to the latest data.

The immediate reasoning behind the growing bank is simple:

An increase in the production and use of low carbon fuel, which creates credits

A simultaneous decrease in the use of gasoline and diesel, which creates deficits

The forces behind these trends are much more complex, but the LCFS is itself one of those forces. For example, the production of renewable diesel (RD) is incentivized by LCFS and now makes up almost 40% of the diesel fuel reported in the program. RD displaces the use of conventional diesel which would otherwise create deficits. As more RD is produced, more credits and fewer deficits will be generated each quarter. And RD happens to be the single largest source of credits in the program, making up about ⅓ of all credits last quarter.

Of course, RD is not the only fuel generating credits and contributing to the growing credit bank…

Q3 2022 Credit Trends

The largest quarter-over-quarter increases came from renewable natural gas (10%), ethanol (6%), and electricity (6%).

RD declined slightly (-3%) for the first time since 2020

The primary driver of credit growth from renewable natural gas (RNG), the third largest credit source in the program, has been declining average CI. While RNG volume is only 7% up from the same quarter last year, the average CI is now -111 gCO2e/MJ compared to -60 last year. The lower the CI of a fuel, the greater number of credits it will generate.

Spotlight on EV Credits

Credits from electric vehicles continue to be a major source of growth in LCFS, reaching a record share of credits generated Q3 2022 (24%). Consistent with previous quarters, almost 90% of credits from EV charging came from just three categories: residential (49%), eForklifts (23%), and non-residential light/medium-duty (15%).

CARB is expected to release Q4 2022 data by April 28, 2023.

The Pasha Group Partners with SRECTrade to Decarbonize through California’s LCFS Program

Pasha Hawaii’s LNG-powered George III on its maiden voyage to Honolulu in August 2023

SAN RAFAEL and SAN FRANCISCO, CA — Today The Pasha Group announced its partnership with SRECTrade to transition to low- and zero-emission equipment across its West Coast operations. The logistics and transportation services leader is partnering with SRECTrade to generate and monetize carbon credits from electric vehicles and equipment under the California Low Carbon Fuel Standard (LCFS).

The Pasha Group has led the transition to renewable energy in the marine ports sector through many projects and initiatives over the last five years, through initiatives to retrofit forklifts, drayage trucks, terminal tractors, and on-road EV trucks in California, the installation of dozens of charging stations, and a microgrid. The company has also conducted Terminal Equipment demonstration and prototyping projects in the Port of Los Angeles and serves on goods movement Technical Advisory Committees for the California Energy Commission. The Pasha Group and its partners have accomplished milestones in the marine port transition to clean energy such as approving and performing the first hydrogen refueling for a hydrogen powered vessel.

The Pasha Group continues to pave the way in electrifying ports with the support from incentives like LCFS, a market-based compliance program that provides ongoing funding to entities operating electric and hydrogen equipment. SRECTrade’s expert advisory and technology-enabled services make participation in complex compliance programs simple, rewarding, and transparent.

“SRECTrade is a valuable partner, providing our team with up-to-date information and opportunities to incorporate sustainability practices into our operations,” says George Pasha, IV, President and CEO. “Our partnership with SRECTrade contributes to our mission of moving forward as quickly as possible with our ESG goals.”

For companies still looking to benefit from clean fuels programs, The Pasha Group advises getting started now and working with a trusted partner like SRECTrade. To learn how much you can earn from clean fuel programs, contact SRECTrade at cleanfuels@srectrade.com.

About The Pasha Group

Established in 1947, The Pasha Group is a family-owned, third-generation diversified global logistics and transportation company that provides ocean transportation for containers and rolling stock between the U.S. West Coast and Hawaii; port processing services for finished and privately owned vehicles; stevedoring for vehicles, breakbulk and container cargos; auto hauling services with its truck fleet throughout the contiguous U.S.; domestic and international relocation services; and international logistics management for general commodity and project cargoes.

About SRECTrade

As the leader in environmental commodity management, SRECTrade provides full-service management and transaction solutions across a variety of renewable energy and clean fuel programs. The company is the largest third-party manager of EV charging assets under the California Low Carbon Fuel Standard. SRECTrade’s parent company, Xpansiv, provides market infrastructure to rapidly scale the world’s energy transition. Xpansiv operates CBL, the largest spot exchange for environmental commodities, including carbon credits and renewable energy certificates.

Tags: lcfs Posted in Low Carbon Fuel Standard | Comments Off on Global Logistics and Transportation Services Leader Paves the Way for Reducing Emissions in the Marine Ports Sector

SRECTrade Pays Fleets under Canada’s Clean Fuel Regulations for Owning and Operating Electric Equipment.

SAN FRANCISCO, CA — SRECTrade, the single partner to manage and transact environmental commodities, announced that it has expanded its management and transaction services to Canada. With these services, SRECTrade and parent company Xpansiv, the premier global market-infrastructure platform for environmental commodities, generate and monetize clean fuel credits to fund budgets to help cover the cost of deploying and operating zero emission vehicles.

In June 2022, Canada launched the Clean Fuel Regulations (CFR), requiring a reduction in the carbon intensity (CI) of transportation fuels by 15% by 2030. This fuel agnostic program provides valuable incentives for transitioning to and operating clean fleets, including EV charging stations, electric and hydrogen buses, trucks and other equipment. The CFR shares many similarities with clean fuel programs across the United States including the California Low Carbon Fuel Standard (LCFS) and Oregon Clean Fuel Program (CFP). To learn more about participating in the Canada CFR, register for SRECTrade’s webinar on January 31 at 10 am PST.

SRECTrade is already serving Canadian companies and multinationals broadening their participation in clean fuel programs. As the largest agent manager of electric vehicle charging and renewable energy assets across North America, the firm’s expansion into Canada solidifies SRECTrade’s continued leadership in the space, providing clients equitable access to clean fuel and renewable energy programs wherever they exist.

“Organizations that act quickly to meet registration deadlines will be among the first to start generating credits this year,” says Steven Eisenberg, Xpansiv’s President of Managed Solutions. Under Canada CFR, there is no retroactive credit generation so the best time to get started is now. To learn more, contact cleanfuels@srectrade.com.

About SRECTrade

SRECTrade is the single partner to source, manage, and transact environmental commodities globally. Founded in 2008, SRECTrade is the largest agent manager of electric (EV) and renewable energy assets across the U.S. With a 99% annual client retention rate, the firm has generated almost a billion dollars in value across more than 64,000 clients while managing over 185,000 clean energy assets on its technology platform. SRECTrade partners with commercial and public entities across a variety of market segments including manufacturing, freight and logistics, warehouse and distribution, maritime, EV charging networks, transit fleets, municipalities, universities, property management companies and others. SRECTrade is a wholly owned subsidiary of Xpansiv, the premier market-based infrastructure platform for environmental commodities.

For information concerning this release, please contact: