On August 22, 2019, Steven Eisenberg, SRECTrade’s Chief Executive Officer, will be speaking at a Voice of the Customer Event hosted by CALSTART, a non-profit organization in the clean transportation industry. The event will focus on the application and deployment of Electric Class 5 Trucks and Yard Tractors. The meeting will take place at the South Coast Air Quality Management District office from 10:00 AM – 2:00 PM.

Steven will speak about the California Low Carbon Fuel Standard (LCFS), a market based program that encourages the adoption of low carbon intensive fuels and vehicles. SRECTrade works with participants across the LCFS market, providing credit portfolio management and transaction services to clean fuel fleet operators and other credit generators.

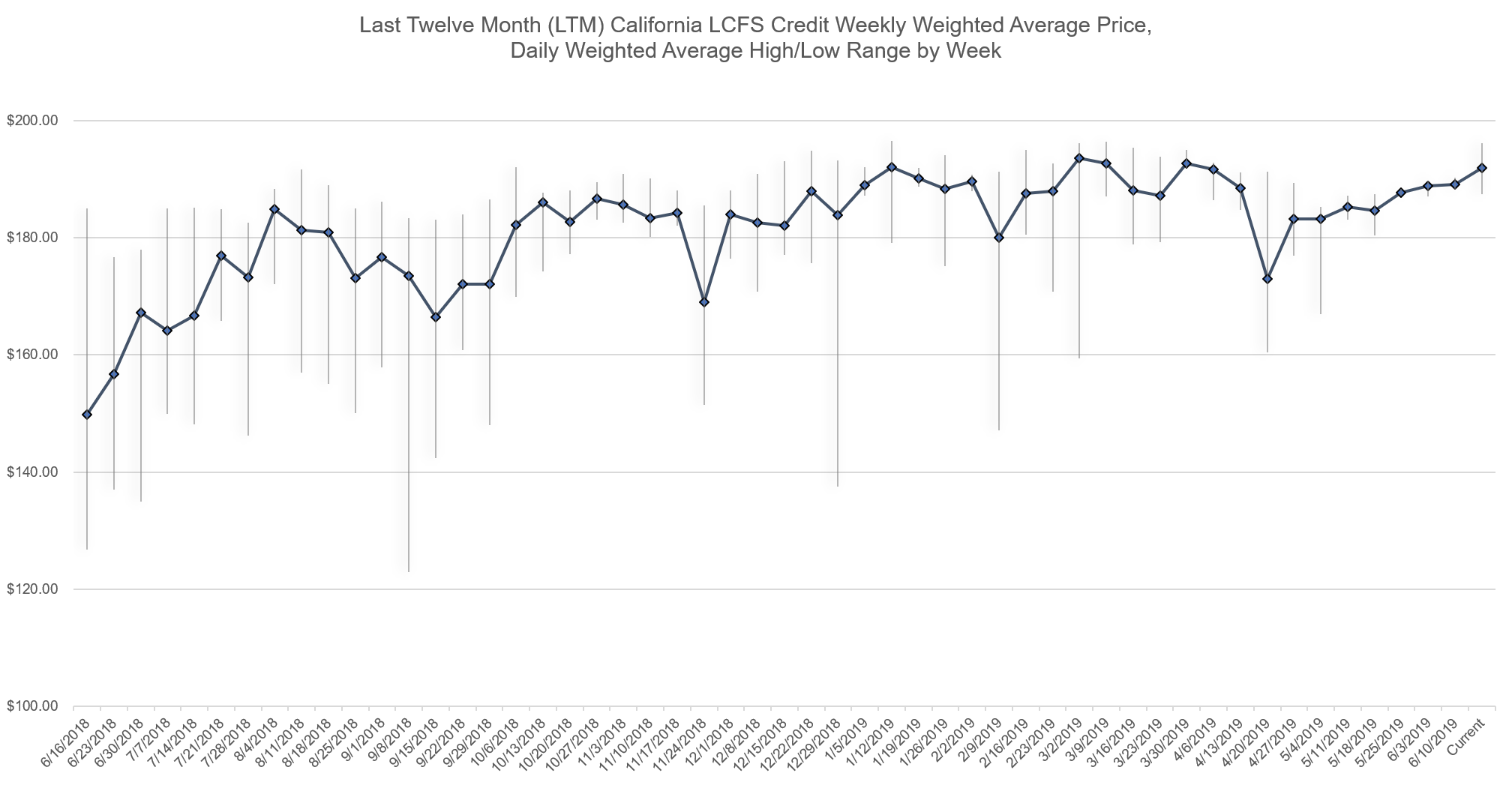

As per data released by the California Air Resources Board (CARB) on July 9th, the California Low Carbon Fuel Standard (LCFS) market saw a slight uptick in pricing this past week, increasing to a weighted average weekly price of $191.67. This is up $1.06 from last week’s average price of $190.61. The market saw a slight decrease in volume this past week with 319,948 credits transferred, down from last week’s volume of 401,628, but up from the last twelve month (LTM) weekly average of 243,170. Credit transfers continue to be high likely due to Q1 credit issuance and associated transfers.

Please click on the pricing chart below for a visualization of LTM trends.

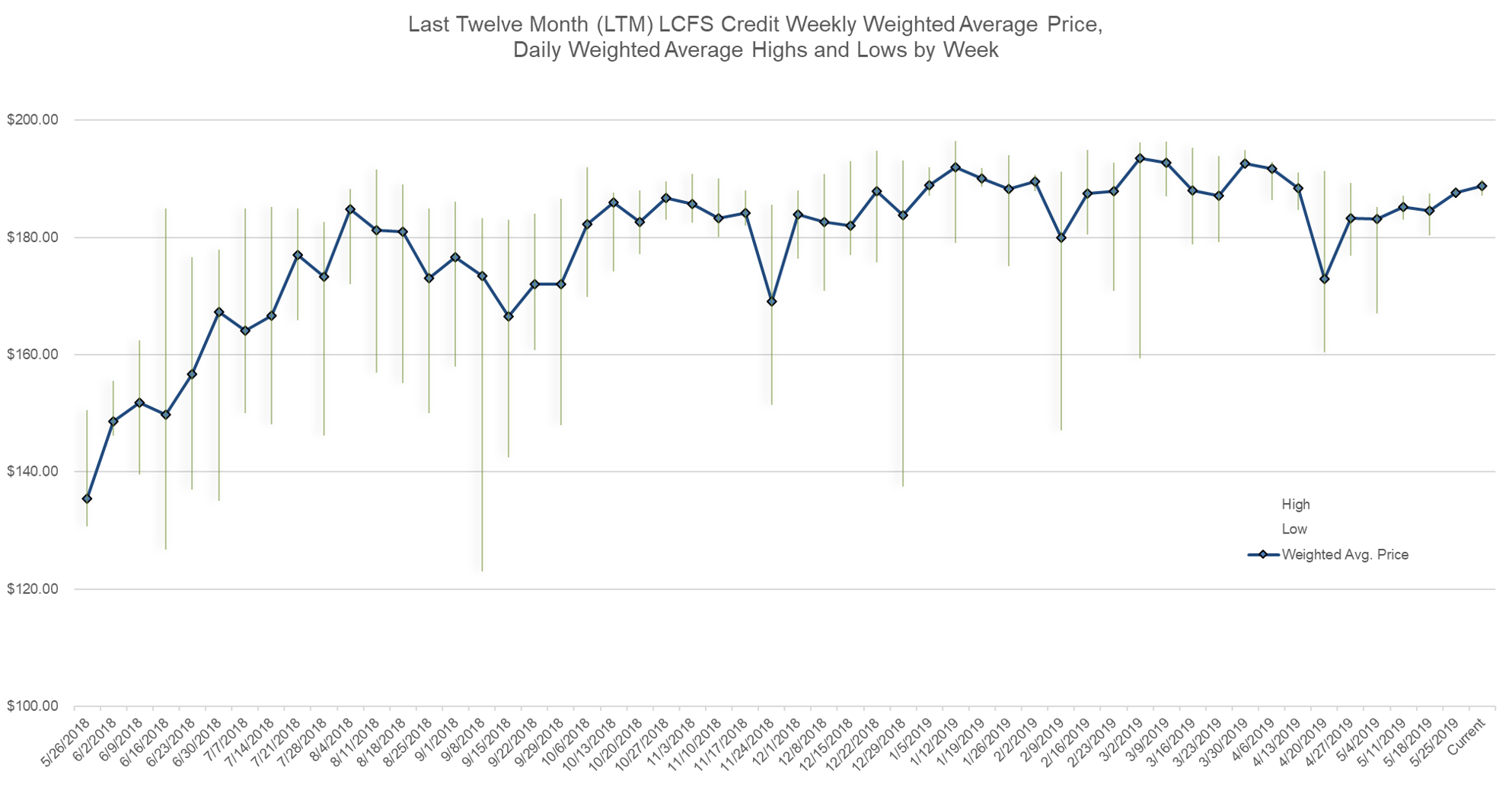

As per data released by the California Air Resources Board (CARB) on July 2nd, the California Low Carbon Fuel Standard (LCFS) market saw a slight drop in pricing this past week, decreasing to a weighted average weekly price of $190.61. This is down $1.26 from last week’s average price of $191.87 and the first week we have seen a price decrease since early May. The market saw a significant increase in volume this past week with 401,628 credits transferred, up from last week’s volume of 39,827 and the last twelve month (LTM) weekly average of 239,704. This is likely due to Q1 credit issuance and associated transfers.

Please click on the pricing chart below for a visualization of LTM trends.

As per data released by the California Air Resources Board (CARB) on June 25th, the Low Carbon Fuel Standard (LCFS) market continued its upward price trend this past week, increasing to a weighted average weekly price of $191.87. This is up $2.75 from last week’s average price of $189.12 and the fourth straight week we have seen an uptick in LCFS pricing. This is also the first time since early April that the market saw pricing above $190 per credit. The market, however, did see a significant decrease in volume this past week with 39,827 credits transferred, down from last week’s volume of 86,403 and the last twelve month (LTM) weekly average of 237,742.

Please click on the pricing chart below for a visualization of LTM trends.

As per data released by the California Air Resources Board (CARB) on June 18th, the Low Carbon Fuel Standard (LCFS) market continued its upward price trend this past week, increasing to a weighted average weekly price of $189.12. This is up $0.28 from last week’s average price of $188.84 and the third straight week we have seen an uptick in LCFS pricing. The market saw a decrease in volume this past week with 86,403 credits transferred, down from last week’s volume of 325,708 and the last twelve month (LTM) weekly average of 241,706.

Please click on the pricing chart below for a visualization of LTM trends.

Source: California Air Resources Board (CARB)Tweet

Posted in Low Carbon Fuel Standard | Comments Off on California LCFS Pricing Update: Market Pricing Hits Eight-Week High

As per data released by the California Air Resources Board (CARB) on June 11th, the Low Carbon Fuel Standard (LCFS) market continued its upward price trend this past week, increasing to a weighted average weekly price of $188.84. This is up $1.78 from last week’s average price of $187.06 and the second straight week we have seen an uptick in LCFS pricing. The market also saw a jump in volume this past week with 325,708 credits transferred, up from last week’s volume of 106,031 and the last twelve month (LTM) weekly average of 243,077.

In recent weeks, we have also seen a decrease in daily price variance over a given week. This indicates a more uniformly priced market and perhaps a steadier volume of credits transacted on a daily basis.

Please click on the pricing chart below for a visualization of LTM trends.

Data Source: California Air Resources Board (CARB)Tweet

On June 13th, Yaniv Lewis, an Environmental Markets Associate at SRECTrade, is speaking at a Voice of the Customer Event hosted by CALSTART, a non-profit in the clean transportation industry. The event, which will be a discussion on Medium and Heavy-Duty Electric Step Vans, will take place at the Clovis Veterans Memorial District in Clovis, CA from 10:00 AM – 2:00 PM.

Yaniv will speak on the Low Carbon Fuel Standard (LCFS) market, a state incentive that encourages the uptake of low carbon intensive vehicles. SRECTrade provides its services to participants across the LCFS market, providing credit portfolio management and brokerage services to clean fuel asset owners and credit generators.

Learn more about the event here and register for free here.

On April 30th, the California Air Resources Board (CARB) released Q4 2018 data on the Low Carbon Fuel Standard (LCFS) market in California. Notably, the market saw an LCFS credit surplus of approximately 67k credits, snapping a deficit streak of four straight quarters. Approximately 3.27 million metric tons (MT) of credits were generated in Q4 2018 compared to 3.20 million MT of deficits in the same time frame. This credit surplus can be largely attributed to the uptick in clean diesel substitutes, namely renewable diesel and bio-diesel, which from a volumetric perspective, increased 37.2% and 14.8%, respectively, from Q3 to Q4 2018.

The following chart shows credit production changes for the highest credit-producing fuels in the LCFS market:

Source: CARB

With an average quarter-over-quarter credit increase rate of 9.11% since Q1 2011, the Q4 2018 increase of 16.89% from Q3 2018 is well above the running average. However, when factoring out the increases in renewable diesel and bio-diesel credit generation, overall credit generation only increased 1.45% from Q3 to Q4 2018. As such, monitoring the influx of renewable diesel and bio-diesel in the marketplace will be integral to projecting credit growth over the next few quarters.

The following chart shows deficit changes for the two baseline deficit-producing fuels in the LCFS market:

Source: CARB

While CARBOB and diesel fuels both saw a volumetric and deficit-production decline in Q4 2018, the influx of renewable diesel into the market produced 160k deficits in Q4 2018. This outpaced the deficit decrease in traditional deficit-producing fuels, increasing the overall deficit count by 2.03% from Q3 2018.

The following chart released by CARB illustrates the overall LCFS market trends:

Source: CARB

With a step down in the Carbon Intensity (CI) Compliance Standard in 2019, we will likely see an uptick in deficit production beginning in Q1 2019, barring any major changes in fuel production. The influx of renewable diesel will continue to be a determining market force from both a credit and deficit perspective.

With regards to pricing, in recent weeks, we have seen pricing come off its ~$200 peak after CARB proposed a hard $200 price cap (in 2016 $ indexed for inflation) on the program in a workshop on April 5th. As of recent, CA LCFS spot market pricing has ranged between $180 and $185/credit.

SRECTrade offers LCFS credit management and brokerage services to electric vehicle (EV) fleet operators, OEMs, EV charging station owners, and other asset owners. We help our clients navigate through the entire LCFS process including asset registration, ongoing reporting requirements, transacting, settlement, and remittance of funds. Our domain expertise in environmental commodity markets allows us to provide our clients with industry leading regulatory and market knowledge. Please reach out to cleanfuels@srectrade.com for more information.

Pursuant to the California Global Warming Solutions Act (AB32), Executive Order S-01-07 of 2007 called for a Low Carbon Fuel Standard (LCFS) to reduce the carbon intensity (CI) of California transportation fuels by 10% by 2020, from a 2010 baseline. The Order instructed the California EPA to develop a compliance schedule and directed the California Air Resources Board (CARB) to initiate regulatory proceedings to implement the program. CARB approved the LCFS regulation in 2009. Implementation and the first year of compliance began in 2011. Revisions to the program were made at the end of 2011 and took effect in 2013. Due to a court ruling that found procedural issues with the original adoption of the program, the program targets were effectively frozen from 2013 – 2015 until CARB re-adopted it in 2015. In January 2019, CARB amended the LCFS regulations and increased the carbon intensity reduction goal to 20% by 2030. An LCFS Credit is issued per 1 metric ton (MT) of CO2 equivalent reduced.

Other states and territories (i.e. Oregon and British Columbia) on the western seaboard of North America have followed in California’s footsteps and implemented LCFS programs of their own. As compliance standards continue to build, these programs hope to stimulate greater regional synergy in lowering greenhouse gas emissions.

Quick Facts

1 LCFS Credit = 1 MT of CO2 equivalent reduced

Electric Vehicle Fleets and Charging Stations must be certified by CARB to sell LCFS credits

Value is determined by market supply and demand mechanics

The LCFS applies to the sale or supply of any fuel in California. Fuel producers and importers are the primary regulated parties. Regulated parties that exceed the maximum CI compliance limit may meet compliance by purchasing credits that are issued to regulated parties with an average CI that is below the maximum CI compliance limit. The LCFS enforces a declining CI curve every year to ensure the continuous reduction of the transportation fuel industry’s environmental impact. The chart below reflects the compliance schedule of average CI that needs to be meet for each respective baseline fuel type.

California Carbon Intensity Compliance Schedule; Source: California Air Resources Board (CARB) Source: California Air Resources Board (CARB)

Pricing

Source: California Air Resources Board (CARB) as of March 10, 2019

SRECTrade’s Clean Fuels Management Services

SRECTrade provides EV charging networks, fleet operators, original equipment manufacturers, and independent EV charging station owners comprehensive fuel credit registration, management and monetization services. We make it easy to register, manage and navigate the regulatory and administrative complexities of the western clean fuels markets. Our company facilitates a return on the investment in your EV fleet or charging station portfolio through low-carbon fuel standard (LCFS) credit management and transaction services. If you are interested in our services or have any questions, please reach out to our Clean Fuels Team at cleanfuels@srectrade.com.