SRECTrade SREC Markets Report: August 2011

The following post outlines the megawatts of solar capacity certified and/or registered to create SRECs in the SREC markets SRECTrade currently serves.

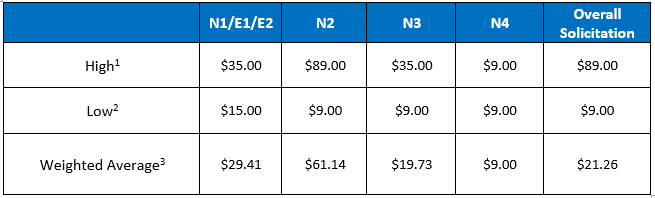

For a PDF copy of this table click here.

PJM Eligible Systems

As of the end of August, there were 18,112 solar PV (17,791) and solar thermal (321) systems registered and eligible to create SRECs in the PJM Generation Attribute Tracking System (GATS) registry. Of these eligible systems, 77 (0.43%) have a nameplate capacity of 1 megawatt or greater, of which only 6 systems are greater than 5 MW. The largest system, currently located in New Jersey, is 18.3 MW, and the second largest, located in Ohio is 12 MW. The third largest system, at 11.2 MW, is located in Delaware.

Beginning of energy year for DE, NJ, and PA

June 1, 2011 marked the beginning of the new energy year for DE, NJ, and PA. All requirements for these markets increase given their RPS solar carve out schedules. SRECs for the month of July, the second creation period for the new reporting year, will be minted at the end of August.

Delaware: The reporting year 2011-2012 requirement for DE equates to approximately 21 MW being online for the entire year or approximately 25,600 SRECs created. As of August 25, 2011, 20.5 MW of solar capacity was registered and eligible to create DE SRECs in PJM GATS. 11.2 MW of the 20.5 MW currently eligible is from the Dover Sun Park project developed by LS Power. In the 2011-12 compliance year, Delmarva Power has contracted to purchase 9,846 SRECs from the project, of which 7,000 are being held by the Sustainable Energy Utility (SEU) until 2015-16*.

New Jersey: The reporting year 2012 requirement for NJ equates to approximately 368 MW being online for the entire year with a fixed SREC requirement of 442,000 MWhs. As of August 25, 2011, 379 MW of solar capacity was registered and eligible to create NJ SRECs in PJM GATS. While this figure represents all projects registered in GATS, there are recently installed projects awaiting issuance of a New Jersey state certification number. This delay results in a portion of installed projects not yet represented in the 379 MW figure. On July 26, 2011 the NJ Office of Clean Energy (NJ OCE) reported that as of June 30, 2011 more than 380 MW (10,086 projects) of solar had been installed in NJ. The news release noted that 40 MW were installed in the month of June. The installation data for July 2011 has not yet been released by the NJ OCE. For more details on the the current NJ market conditions see this post.

Pennsylvania: The reporting year 2012 requirement for PA equates to approximately 44 MW being online for the entire year or approximately 53,000 SRECs created. As of August 25, 2011, 124.5 MW of solar capacity was registered and eligible to create PA SRECs in PJM GATS.

Massachusetts DOER Qualified Projects

As of August 15, 2011, there were 861 MA DOER qualified solar projects; 829 operational and 32 not operational. Of these qualified systems, 11 (1.3%) have a nameplate capacity of 1 megawatt or greater, of which only 3 are between 1.5 and 2 MW. Three of the projects greater than 1 MW are currently operational.

Capacity Summary By State

The tables above demonstrate the capacity breakout by state. Note, that for all PJM GATS registered projects, each state includes all projects certified to sell into that state. State RPS programs that allow for systems sited in other states to participate have been broken up by systems sited in state and out of state. Additional detail has been provided to demonstrate the total capacity of systems only certified for one specific state market versus being certified for multiple state markets. For example, PA includes projects only certified to sell into the PA SREC market, broken out by in state and out of state systems, as well as projects that are also certified to sell into PA and Other State markets broken out by in state and out of state systems (i.e. OH, DC, MD, DE, NJ). PA Out of State includes systems sited in states with their own state SREC market (i.e. DE) as well as systems sited in states that have no SREC market (i.e. VA). Also, it is important to note that the Current Capacity represents the total megawatts eligible to produce and sell SRECs as of the noted date, while the Estimated Required Capacity – Current and Next Reporting Year represents the estimated number of MW that need to be online on average throughout the reporting period to meet the RPS requirement within each state. For example, New Jersey needs approximately 368 MW online for the entire 2012 reporting year to meet the RPS requirement. Additionally, the data presented above does not include projects that are in the pipeline or currently going through the registration process in each state program. This data represents specifically the projects that have been approved for the corresponding state SREC markets as of the dates noted.

*Source: State of Delaware Pilot Program For the Procurement of Solar Renewable Energy Credits: Recommendations of the Renewable Energy Taskforce