On November 8th, the California Air Resources Board (CARB) approved the proposed updates to the Low Carbon Fuel Standard (LCFS) regulation. This approval is the culmination of a two-year rulemaking process which saw passionate input from a diverse range of stakeholders. The updated regulation will set more ambitious carbon reduction standards and increase the stringency of credit qualifications, to ensure long-term integrity in the program.

We’ve provided a summary of the key updates to the regulation, focusing on electric fleets and EV networks. You can also find more detailed information on the rulemaking website.

Next Steps and Implementation Timeline

CARB is anticipated to complete their final rulemaking documents by early January and submit them to the State’s Office of Administrative Law. From there, the administrative office will review the entire rulemaking process and the amendments to ensure compliance with California law. If everything meets the necessary requirements, the updates to the regulation will go into effect on April 1, 2025. However, it’s important to note that some amendments, such as forklift metering and verification requirements, have specific delayed implementation dates to give businesses time to adapt to the new requirements (see below).

More Aggressive Carbon Intensity Standard

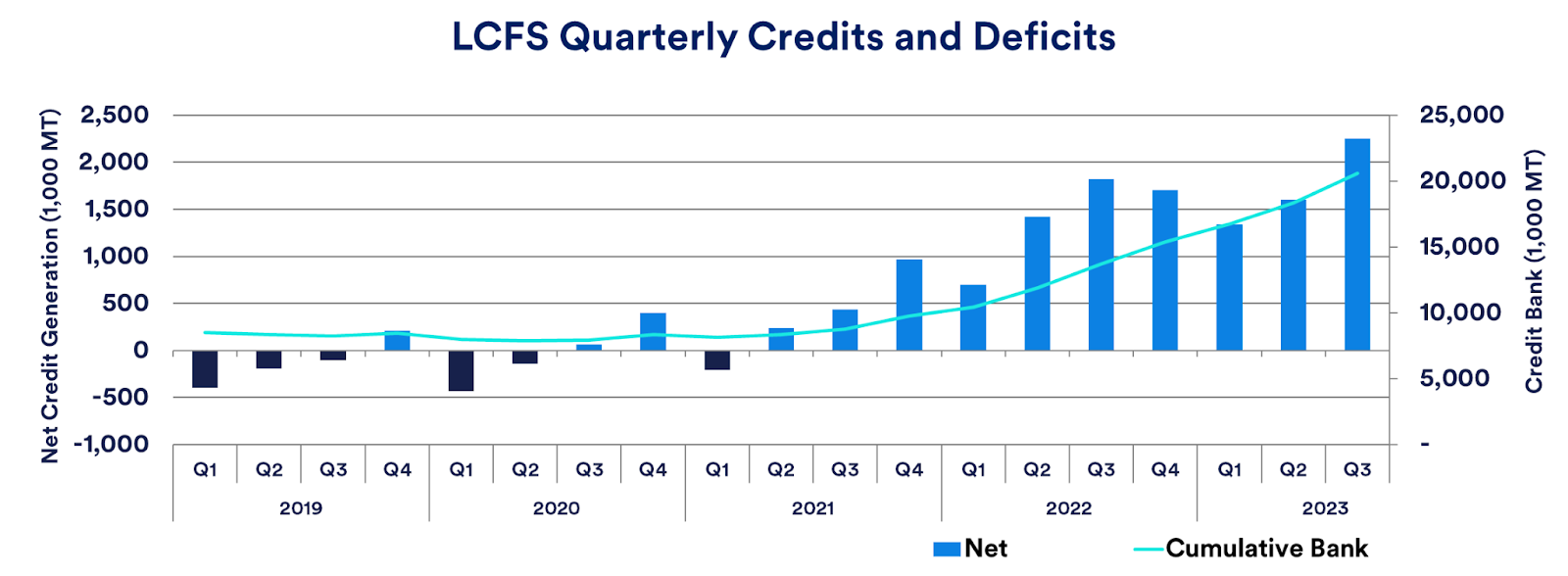

CARB has tightened the Carbon Intensity (CI) standard, making the carbon reduction goals more ambitious than previously required, with a large single-year drop in CI Standard in 2025. This adjustment is CARB’s most significant lever to increase the value of Low Carbon Fuel Standard (LCFS) credits and encourage long-term participation in the program. This change is already leading to increased LCFS credit values in the market.

Additionally, the amendments introduce an Automatic Adjustment Mechanism starting in 2028. This new tool will set criteria that automatically trigger a tighter CI standard when credit supply volumes hit a certain threshold. This improvement allows the market to adapt much quicker than in the past, leading to more stable credit values in the long-term.

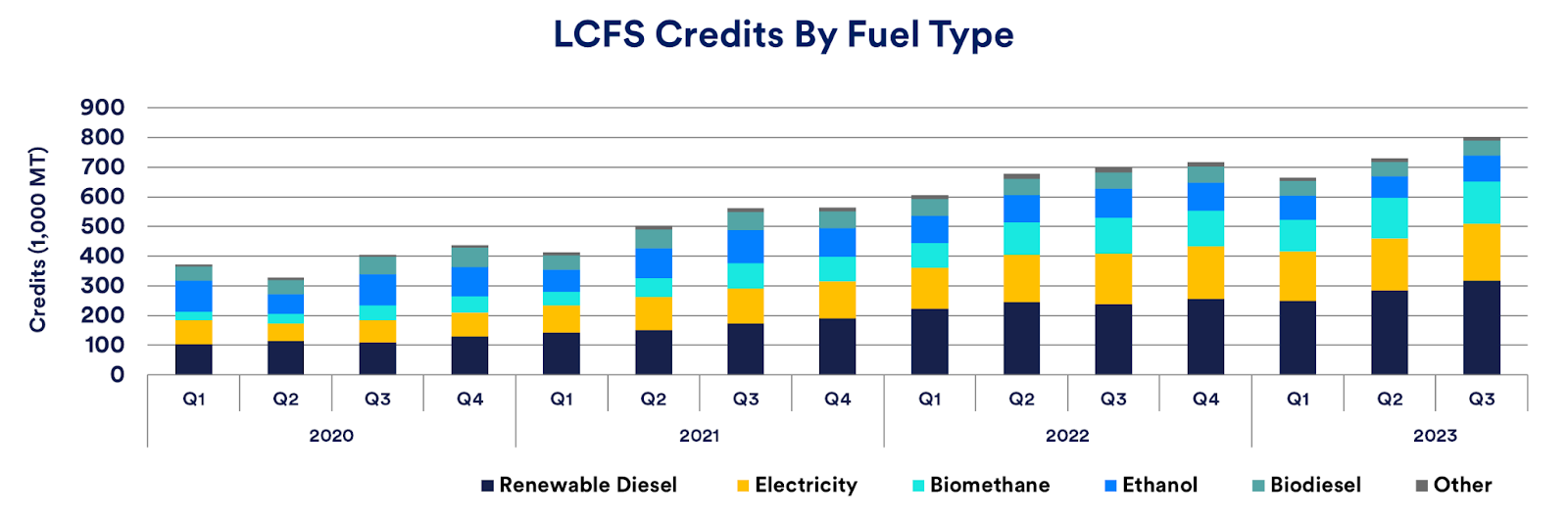

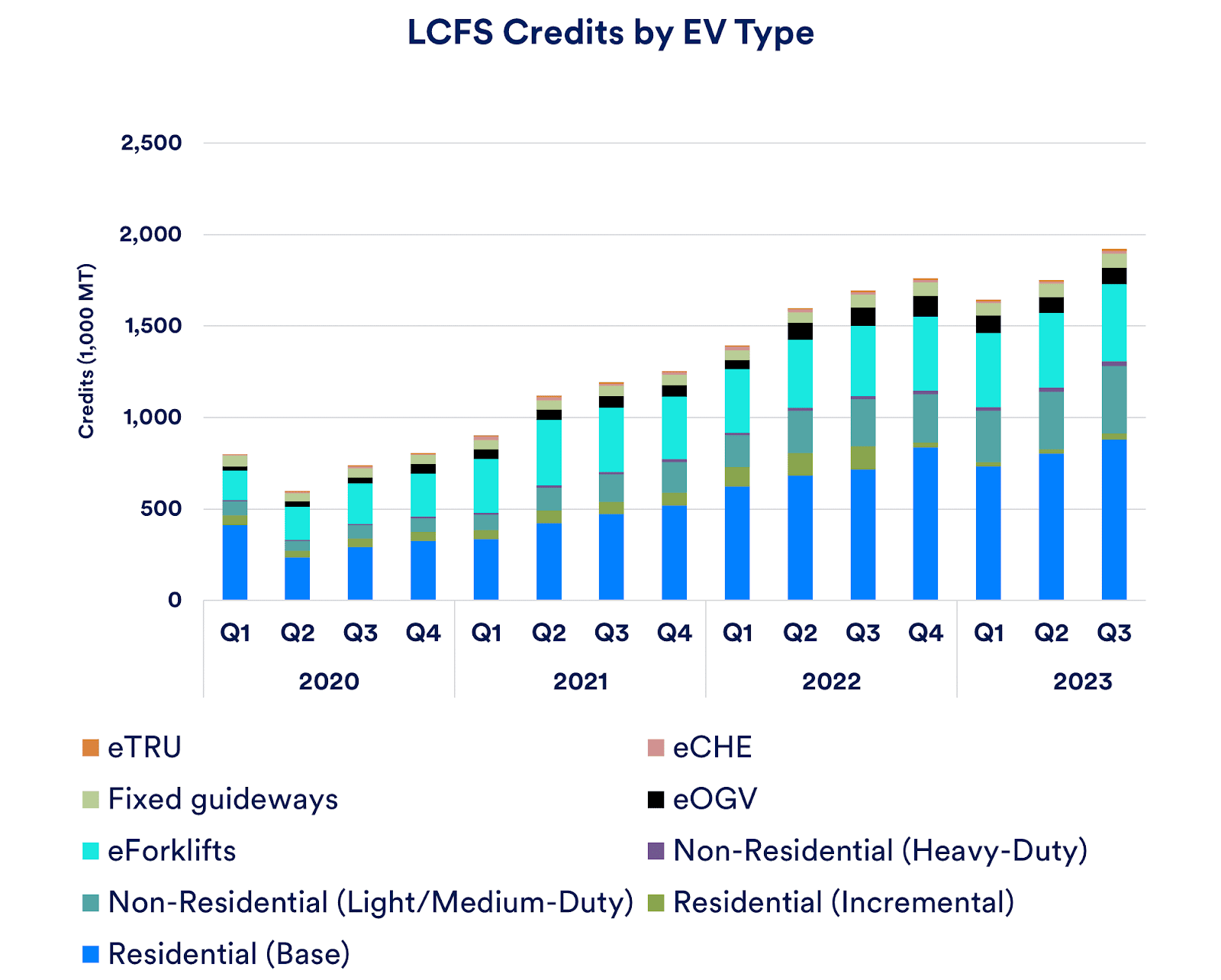

Updates for Electric Forklifts

Energy Economy Ratio (EER)

Once the regulation updates are implemented, forklifts will no longer be segregated by model year for reporting. However, all forklifts with a capacity of less than 12,000 lbs (the majority of the deployed electric forklift population) will see a 37% decrease in the Energy Economy Ratio (from 3.8 to 2.4). This means fewer credits will be generated per amount of electricity used.

Forklift Metering will be required in 2026

Starting in 2026, forklifts will no longer be allowed to estimate energy usage. Instead, fleets will need to measure the energy used to charge forklifts, bringing forklifts in line with all other categories of electric vehicles (EVs). SRECTrade has a cost-effective forklift metering solution for our partners, which are already being deployed in Oregon, Washington and Canada and will provide more information to our partners as this deadline approaches.

New Opportunity to generate revenue for charging electric Transport Refrigeration Units (eTRUs)

The right to generate credits for charging eTRUs has changed so that the owner of the facility where the eTRU charger is located can claim the credits. Previously, the regulation gave the right to report credits to the owner of the eTRU. As with other electric vehicle reporting, it is necessary to measure the energy use at the eTRU charger in order to generate credits. For entities that participated under the previous regime, they can continue to generate credits if they own the facilities where their eTRUs are charged, or they can work with the facility owner to arrange a pass through of credit reporting rights.

Verification of Reporting

Historically, EV Charging data has been exempt from third party verification requirements under the LCFS program. However, starting with electricity used in 2026, LCFS credits from using electricity for fuel (including EV Charging, e-forklifts, eTRUs, etc.) will be subject to verification. Verification is completed after the reporting is submitted to the regulator; for example, for all 2026 reporting, verification work will be completed in early 2027. SRECTrade has experience in successfully navigating verification and auditing processes and will reach out to our partners with more details on what to expect with verification as the implementation date approaches.

Feel free to reach out to the SRECTrade Clean Transportation Team (cleanfuels@srectrade.com) if you have any questions or need further clarification on any of these points!